Self-Directed IRAs Are Opening Retirement Accounts to Real Estate and Private Markets

A growing number of investors want their retirement dollars doing more than tracking the S&P 500 — and a lesser-known account type is how they're getting there. As a recent Investor's Business Daily feature lays out, the self-directed IRA (SDIRA) lets investors hold real estate, private equity, precious metals, and other assets that never trade on a public exchange — all inside the same tax-advantaged wrapper as a traditional or Roth IRA. With $19.2 trillion sitting in IRAs at the end of 2025, per the Investment Company Institute, even a modest shift toward alternatives represents an enormous pool of capital looking for a home.

The Push Beyond Stocks and Bonds

The appetite for diversification is broadening well past institutions. Recent run-ups in bitcoin, gold, and silver have put the case for non-correlated assets back in the spotlight, and investors are increasingly looking for exposure that doesn't move in lockstep with public equities. Policy is leaning the same direction — IBD notes that an August 2025 executive order paved the way for private investments inside employer-sponsored retirement plans, though IRAs were left out of that order. Wall Street is responding too: brokerages such as Charles Schwab are opening access to alternative assets like REITs, real estate syndications, and private funds for retail clients. The SDIRA offers a different route into the same trend — one built around direct ownership of a specific asset rather than selection from a curated fund menu.

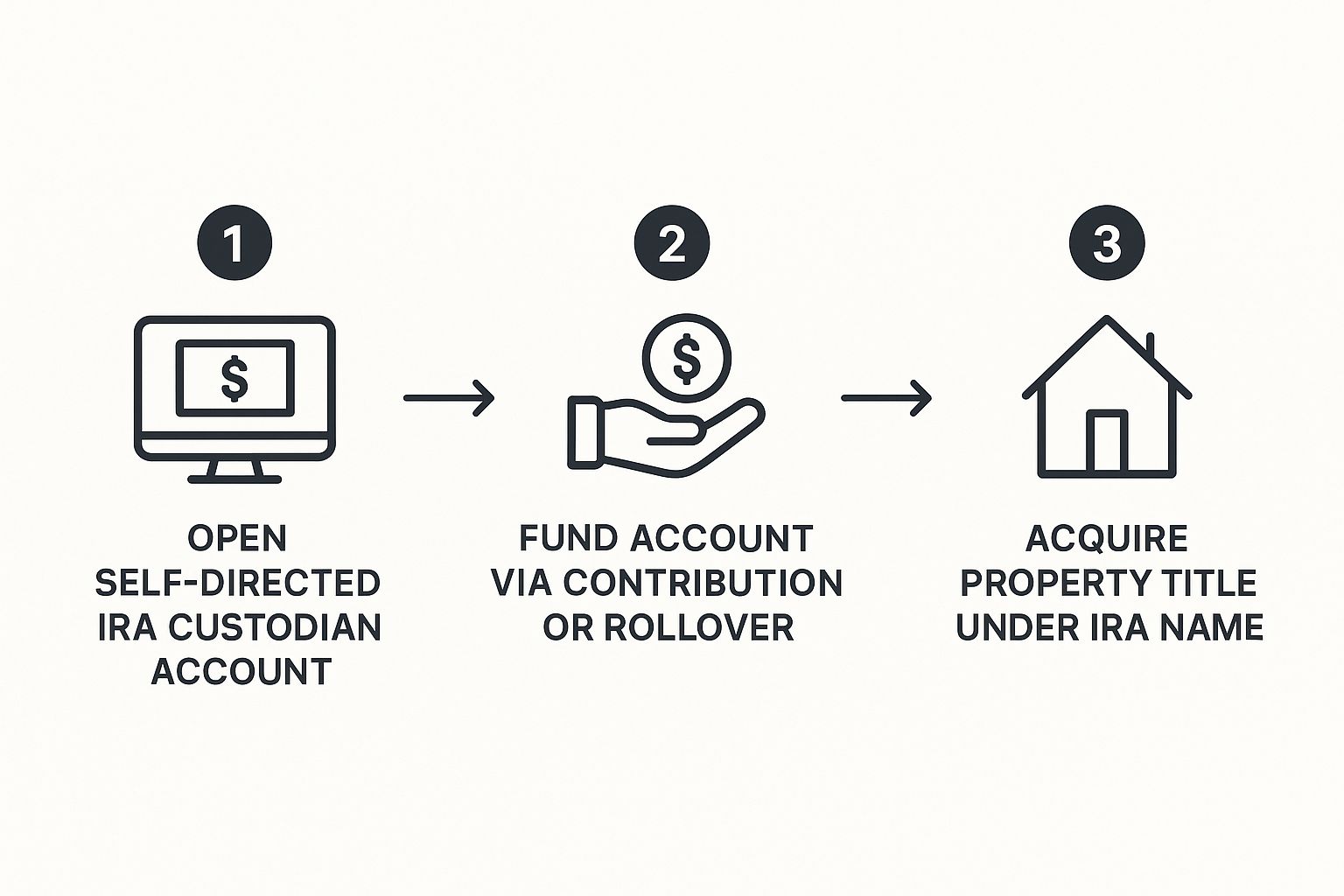

How a Self-Directed IRA Actually Works

The SDIRA carries the same tax treatment as any other IRA, with one defining difference: a much larger menu. "You have much more control over how your money is invested compared to a standard IRA," The Entrust Group's Tony Unkel told IBD. The catch is that you can't open one at Fidelity, Vanguard, or T. Rowe Price — those firms support only publicly traded holdings. An SDIRA requires a specialized custodian that explicitly handles private assets. The IRS allows a wide range inside the account: real estate across residential, commercial, and land; precious metals held in an approved depository; private equity; peer-to-peer lending; and cryptocurrencies. Life insurance, S-corporation shares, and collectibles like art and most coins are off-limits, as is any "self-dealing" between the account and its owner.

The Money Can Move Without a Tax Hit

Funding an SDIRA works three ways. Investors can make an annual contribution — capped at $7,500 in 2026, or $8,600 for those 50 and older — but the bigger levers are rollovers and transfers. Rolling over an old 401(k) or moving funds from an existing brokerage IRA carries no IRS dollar limit, which is what makes larger purchases like real estate feasible. "Rollovers and account transfers are not contributions, so there is no dollar limit," Unkel noted. That mechanic is the practical key: it lets an investor assemble enough capital inside the account to fund a real deal.

The Trade-Off Is Responsibility

The flexibility comes with a heavier lift. SDIRA custodians are not fiduciaries — they hold assets and execute instructions, but they don't give advice, make recommendations, or vet deals. "In a self-directed IRA, the important word is 'self' — you're doing everything yourself," Unkel said. Private assets are also less liquid, less transparent, and carry higher fees than public funds. U.S. Bank's Kaush Amin suggests alternatives suit investors with a 15-year-plus horizon and that a meaningful allocation — he points to a 10% minimum — is needed to move the needle. The repeated refrain from the professionals: due diligence, due diligence, due diligence.

The Bigger Picture

Alternatives are shedding their reputation as an institutions-only allocation and becoming a standard tool for diversification — and the structures that make private-market access genuinely available are the ones that will capture the shift. When a mainstream brokerage like Schwab moves to put REITs, real estate, and private funds in front of retail clients, it's a clear signal that the category has gone from fringe to expected. The SDIRA is one of the most direct of those structures, especially for real estate, which sits squarely on the IRS's approved list. The momentum is toward broader participation; the real gating factor is no longer appetite but knowing how to access it responsibly.

For Neighborhood Ventures, this is exactly the access we were built to provide. Individual investors can fund NV real estate offerings through self-directed IRAs using custodians like Directed IRA and Equity Trust — putting retirement dollars to work directly in Phoenix multifamily real estate — choosing the specific asset rather than selecting from a brokerage's curated fund shelf. That's the kind of access we think more investors deserve.

About the author

Neighborhood Ventures